Asia's arms race: India, Pakistan, and Gulf states drive the market

According to the latest report from the Stockholm International Peace Research Institute, international arms transfers increased by 9.2 per cent between 2021 and 2025. Excluding the war in Ukraine, Asia remains the main source of global demand, driven by the rivalry between India and Pakistan and tensions with China. Saudi Arabia, Qatar, and Kuwait are in the top.

Milan (AsiaNews) – A new report from the Stockholm International Peace Research Institute (SIPRI) found that, except for Ukraine, Asia is now the centre of global arms demand.

The study, based on international arms transfers for the period 2021-2025, notes that the global volume of arms transfers between states increased by 9.2 per cent over the previous five-year period, the most significant growth since 2011-2015.

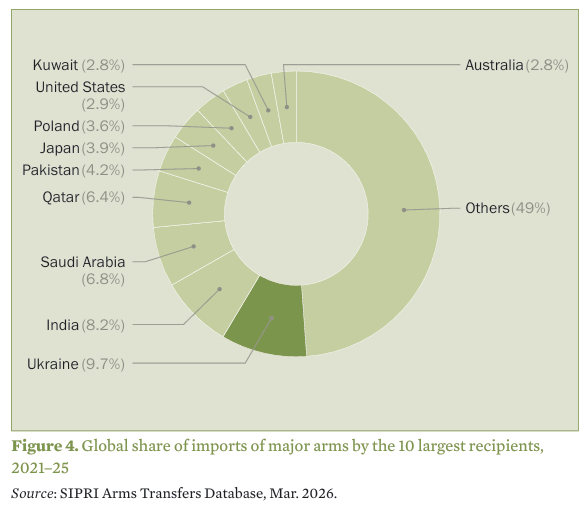

The main buyers are Ukraine, India, Saudi Arabia, Qatar, and Pakistan, which together receive approximately 35 per cent of global imports. While Ukraine's top spot is directly linked to the war with Russia, the rest highlight the centrality of Asia and the Middle East in the arms race.

In the period 2021-2025, Asian states accounted for 31 per cent of global arms imports, second only to European states. Four of the ten largest global importers are in Asia and Oceania, namely India, Pakistan, Japan, and Australia.

Demand for military hardware in Asia is fuelled by competition between India and Pakistan, tensions between India and China, and the confrontation between Beijing and other East Asian countries.

India was the world's second-largest importer of heavy weapons in the period 2021-2025, with an 8.2 per cent share of global imports. New Delhi's military acquisitions are a consequence of tensions with Pakistan and China, rivals with whom it had armed clashes over decades, the latest in May last year.

Despite this, compared to the previous five-year period (2016-2020), Indian imports decreased by 4 per cent, due to India's growing capacity to design and manufacture weapons systems domestically. Significant delays often occur, forcing India to rely on foreign suppliers.

While New Delhi’s dependence on Moscow has dropped significantly – from 70 per cent in the 2011-2015 period to 51 per cent in 2016-2020, and 40 per cent in the 2021-2025 period, Russia remained India’s main supplier, with France coming in second place with 29 per cent, followed Israel with 15 per cent.

At present, based on outstanding orders, 140 French fighter aircraft and six German submarines are expected to arrive in India soon.

Pakistan was the world's fifth-largest arms importer, accounting for 4.2 per cent of global imports, up by five places in the global arms trade rankings. Its imports increased by 66 per cent between 2016-2020 and 2021-2025, with approximately 80 per cent coming from China.

SIPRI notes that the rivalry between nuclear powers India and Pakistan is the main driver behind the militarisation of South Asia.

In other parts of the continent, import trends vary greatly from region to region. Overall, between 2016-2020 and 2021-2025, arms imports dropped by 31 per cent in East Asia, 28 per cent in Oceania, and 30 per cent in Southeast Asia.

These figures do not indicate a process of disarmament, but rather a growing capacity of some countries to independently develop and manufacture heavy weapons systems. This is the case of South Korea and China, which are now outside the top ten importing countries for the first time since 1991-1995. Compared to five years ago, China’s imports are down by 72 per cent.

Japan is a notable exception. Imports jumped by 76 per cent, propelling the country from eleventh to sixth place in the ranking of largest importers in ten years.

Among other regional players, Taiwan's arms imports rose by 54 per cent, although the country still represents a small share of the global market, 0.8 per cent of global imports.

In Southeast Asia, Indonesia was the leading recipient of heavy weapons, accounting for 1.5 per cent of global imports, followed by the Philippines, Singapore, and Thailand.

Regional conflicts continue to influence arms demand. During recent armed clashes, Cambodia and Thailand used imported weapons. Cambodia used multiple rocket launchers from China, while Thailand used fighter jets purchased from Sweden and the United States, equipped with South Korean-made guided bombs.

While the situation is different in the Middle East, the region represents a major source of global arms demand. Imports decreased by 13 per cent between 2016-2020 and 2021-2025, but three Mideast countries are among the top ten global importers: Saudi Arabia (third place), Qatar (fourth), and Kuwait (ninth).

Although its purchases dropped by 31 per cent between 2016-2020 and 2021-2025, Saudi Arabia remains one of the world’s largest arms buyers, accounting for 6.8 per cent of global imports.

Conversely, Qatar recorded a sharp increase in imports (+106 per cent), while Kuwait’s ranking rose from 47th to ninth with an increase of over 800 per cent.

Over half of the weapons imported by countries in the region come from the United States (54 per cent) followed by Italy (12 per cent), France (11 per cent), and Germany (7.3 per cent).

Regional conflicts, as evinced by the war launched by Israel and the United States against Iran, influence demand. Over the past five years, Israel has relied primarily on imported weapons, while Iran has relied on domestically made missiles.

According to SIPRI, between 2021 and 2025, Israeli imports increased by 12 per cent, making the country the fourteenth-largest importer in the world with the United States as the main supplier (68 per cent), followed by Germany with 31 per cent.

.png)

16/06/2025 16:46

17/06/2024 17:52

27/04/2020 16:04

02/09/2025 19:51